By Brian French |April 4, 2026 | SOUTH FLORIDA SMALL BUSINESS TAX GUIDE · 2025 TAX YEAR

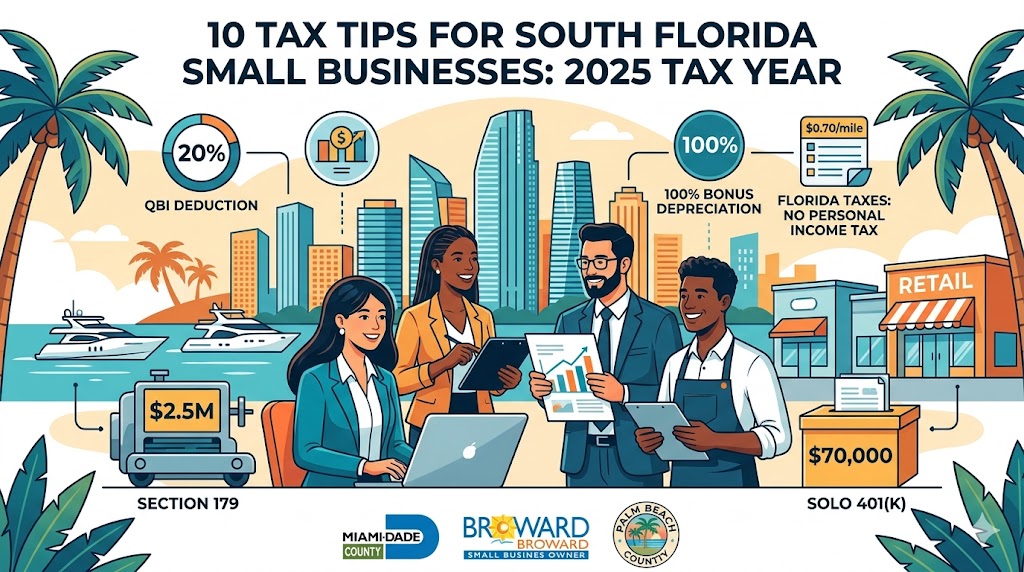

10 Tax Tips Every South Florida Small Business Owner Needs for the 2025 Tax Year

New Federal Law Changed the Rules — Here Is What You Need to Know Before You File

Important notice: This article is provided for general informational purposes only and does not constitute legal, accounting, or tax advice. Every business situation is different. Consult a qualified CPA or tax professional before making any decisions based on this information.

The 2025 tax year is unlike any that has come before it for small business owners. In July 2025, the One Big Beautiful Bill Act (OBBBA) was signed into law, restoring and permanently expanding some of the most valuable tax provisions available to small business owners — provisions that were either phasing out, set to expire, or entirely gone. At the same time, Florida’s unique tax environment — no state personal income tax, a 5.5% corporate income tax that applies only to certain entity structures, and a range of state-specific credits available to qualifying businesses — creates both advantages and responsibilities that South Florida small business owners must navigate carefully.

Whether you run a boutique in Boca Raton, a marine services company in Fort Lauderdale, a real estate team in Miami, or a professional practice anywhere in Broward or Miami-Dade County, these ten tips are designed to help you approach your 2025 return with clarity, confidence, and the full benefit of the deductions and credits available to you.

TIP 1: CLAIM THE 20% QUALIFIED BUSINESS INCOME DEDUCTION — IT IS PERMANENT NOW

If you operate as a sole proprietor, a single-member LLC, a partnership, or an S corporation, you may be eligible for one of the most powerful deductions available to small business owners: the Qualified Business Income (QBI) deduction under Section 199A of the tax code. This deduction allows eligible pass-through business owners to deduct up to 20% of their qualified business income from their federal taxable income — a reduction that, depending on your tax bracket, can save thousands of dollars on your 2025 return.

Before the OBBBA was signed in July 2025, this deduction was set to expire at the end of 2025, creating enormous uncertainty for business owners trying to plan beyond this tax year. The OBBBA made the QBI deduction permanent, eliminating that uncertainty and allowing South Florida small business owners to build their long-term tax strategy around it with confidence.

For the 2025 tax year specifically, the income thresholds work as follows: if your taxable income is at or below $394,600 (married filing jointly) or $197,300 (single), you may be eligible for the full 20% deduction. A phase-in range applies above those thresholds, and certain Specified Service Trade or Business owners (lawyers, doctors, consultants, financial advisors, and others) face additional limitations at higher income levels.

The OBBBA also widened the phase-in ranges — good news for business owners whose income falls in the transition zone — and introduced a new $400 minimum deduction for any qualifying business owner with at least $1,000 in QBI who materially participates in their business, starting in 2026.

What to do: Pull your 2025 income figures together and have your CPA run the QBI calculation for your specific situation. Retirement contributions, health insurance deductions, and entity structure all affect the QBI calculation in ways that a qualified professional can optimize. Do not skip this deduction by assuming you do not qualify.

TIP 2: TAKE FULL ADVANTAGE OF 100% BONUS DEPRECIATION — IT CAME BACK IN 2025

If your business purchased equipment, machinery, vehicles, computers, furniture, or other qualifying personal property after January 19, 2025, you may be eligible to deduct 100% of the cost in the 2025 tax year rather than spreading it over multiple years through traditional depreciation schedules.

Bonus depreciation — first introduced at 100% under the Tax Cuts and Jobs Act — had been phasing down prior to the OBBBA. In 2023, it was 80%. In 2024, it fell to 60%. In 2025, without the OBBBA, it was headed to 40%. The OBBBA permanently restored it to 100% for qualifying property acquired and placed in service after January 19, 2025. For property placed in service between January 1 and January 19, 2025, the rate was 40%.

Unlike Section 179 (see Tip 3), bonus depreciation has no annual dollar limit and can create a net operating loss that may be carried forward to offset future income. It applies to both new and used property, as long as the property is new to your business and acquired from an unrelated party.

For South Florida businesses in industries with significant capital assets — marine services, construction, restaurant equipment, professional office equipment, technology — this provision represents a genuinely transformative tax planning opportunity. A $180,000 piece of equipment purchased in August 2025 can be deducted in full on your 2025 return rather than being depreciated over its useful life.

What to do: Compile a complete list of all property your business acquired and placed in service in 2025. Note the acquisition dates carefully — the January 19, 2025 dividing line matters. Work with your CPA to determine whether bonus depreciation, Section 179, or a combination of both produces the optimal result for your business’s taxable income situation.

TIP 3: USE SECTION 179 TO IMMEDIATELY EXPENSE MAJOR EQUIPMENT PURCHASES

Section 179 of the tax code allows businesses to deduct the full purchase price of qualifying equipment and software in the year it is placed in service, rather than depreciating the cost over several years. The OBBBA significantly expanded this provision for 2025: the Section 179 deduction limit increased to $2.5 million, with a phase-out threshold of $4 million of qualifying property placed in service during the year.

Qualifying property includes machinery, equipment, business vehicles, computers, off-the-shelf software, office furniture, and — importantly for many South Florida business owners — certain nonresidential building improvements such as roofs, HVAC systems, fire protection systems, and security systems. This last category is particularly relevant for business owners who have upgraded their commercial space, improved storm resilience on their building, or invested in security infrastructure during 2025.

One important distinction between Section 179 and bonus depreciation: Section 179 deductions cannot exceed your business’s taxable income for the year. If the deduction would push you into a loss, the excess is carried forward. Bonus depreciation, by contrast, can create a net operating loss. Your CPA can help you decide which tool — or which combination — produces the best outcome for your specific situation.

What to do: Document every major equipment and property improvement purchase made during 2025 with receipts, invoices, and placed-in-service dates. Discuss with your CPA whether Section 179, bonus depreciation, or standard depreciation produces the optimal deduction given your business’s income for the year.

Related Insights

Mastering your tax strategy for 2025 is a critical step in securing your business’s financial future, but building a dominant presence in the South Florida market requires a multi-faceted approach. Beyond the numbers, local firms must focus on establishing geographic relevance to capture digital authority and connecting with the broader community of South Florida business leaders who shape our regional economy. Success also hinges on the mental discipline to overcome negativity bias that can stifle innovation, while leveraging modern tools like a professional Substack newsletter to maintain direct communication with your audience.

TIP 4: MAXIMIZE YOUR RETIREMENT PLAN CONTRIBUTIONS BEFORE THE FILING DEADLINE

Contributions to tax-advantaged retirement plans are one of the most powerful and most consistently underutilized deductions available to South Florida small business owners. Every dollar contributed to a qualifying plan reduces your taxable income dollar for dollar — and unlike many other deductions, retirement contributions can often be made after December 31, 2025, up to the tax filing deadline (including extensions), allowing you to know your exact income for the year before determining the optimal contribution amount.

The 2025 limits are significant. For a Solo 401(k), the combined employee and employer contribution limit is $70,000 for 2025, with an additional $7,500 catch-up contribution available for business owners age 50 or older — and a special enhanced catch-up of up to $11,250 for those ages 60 through 63 under the SECURE 2.0 Act. For a SEP IRA, employers can contribute up to 25% of compensation or $70,000, whichever is less. SIMPLE IRAs have a lower contribution limit of $16,500 for employee deferrals.

For South Florida business owners who are structured as sole proprietors, single-member LLCs, or S corporations, a Solo 401(k) offers the greatest flexibility: it accepts both employee deferrals and employer contributions, allowing a self-employed owner with sufficient net earnings to potentially shelter a substantial portion of their income from federal taxation in a single tax year. Retirement contributions also reduce the QBI calculation in ways that can cascade additional tax savings.

What to do: If you do not yet have a business retirement plan, set one up before the year-end deadline for the plan type you choose (SIMPLE IRAs must be established by October 1 of the year for which you want to make contributions). If you have an existing plan, calculate your optimal contribution amount based on your 2025 income and make the contribution before the filing deadline.

TIP 5: KNOW YOUR FLORIDA ENTITY STRUCTURE — IT DETERMINES YOUR STATE TAX OBLIGATIONS

Florida has no state personal income tax — one of the most frequently cited advantages of running a business here. But whether your business owes state-level taxes depends significantly on how it is structured, and understanding the distinction is essential for accurate compliance and effective planning.

Sole proprietors, partnerships, and S corporations pay no Florida corporate income tax. Their income passes through to the owner’s personal return, which is subject to federal income tax but not Florida state income tax. This pass-through structure is one of the primary reasons many South Florida professionals and small business owners choose the LLC taxed as a partnership or S corporation route.

C corporations, by contrast, are subject to Florida’s corporate income tax at a rate of 5.5% of federal taxable income — but with an important carve-out: the first $50,000 of taxable income is exempt. This means a Florida C corporation with net income of $80,000 effectively pays Florida corporate income tax only on $30,000 of that income. File Form F-1120 by the first day of the fifth month after your tax year ends.

For businesses that have recently restructured, added partners or shareholders, or grown significantly, the question of whether the current entity structure is still tax-optimal deserves a fresh review. An S corporation election, for example, can significantly reduce self-employment tax exposure for owner-operators who pay themselves a reasonable salary — a strategy that is particularly valuable for South Florida service business owners with strong margins.

What to do: Confirm your current entity structure with your CPA and specifically ask whether it remains optimal given your 2025 income level, growth trajectory, and the new QBI deduction rules under the OBBBA. If you have been operating as a sole proprietor and your net income has grown substantially, the S corporation structure deserves a serious conversation.

TIP 6: DEDUCT EVERY LEGITIMATE BUSINESS EXPENSE — AND BUILD THE RECORDS TO PROVE IT

South Florida’s business culture — a world of client lunches at Las Olas restaurants, waterfront meetings, boat-up client entertainment, networking events at yacht clubs, and a professional lifestyle that genuinely intersects with the state’s extraordinary leisure infrastructure — creates both opportunities and responsibilities in the expense deduction category that deserve careful attention.

Business meals with clients and prospects are deductible at 50% when the meal has a genuine business purpose and is properly documented. That documentation must include the date, the business purpose of the meal, the names and business relationships of the attendees, and the amount. A receipt alone is insufficient — the IRS expects contemporaneous records that establish the business context. For South Florida professionals who conduct a significant portion of their relationship-building over meals, this deduction can be substantial if properly tracked.

Vehicle expenses — whether at the standard IRS mileage rate of 70 cents per mile for 2025 or at actual expense — require a mileage log that records the date, the destination, the business purpose, and the number of miles for every business trip. The IRS scrutinizes vehicle deductions heavily, and an undocumented mileage claim is a claim at risk.

Home office deductions — available when a dedicated space is used regularly and exclusively for business — can be claimed either at $5 per square foot (simplified method, maximum 300 square feet) or at the actual percentage of home expenses attributable to the office. In South Florida’s elevated real estate market, the actual expense method often produces a larger deduction.

What to do: Implement a systematic expense tracking system — accounting software, a dedicated business credit card, and a mileage tracking app — that captures business expenses as they occur rather than reconstructing them at tax time. The quality of your records directly determines the defensibility of your deductions.

TIP 7: MAKE QUARTERLY ESTIMATED TAX PAYMENTS — AND DO NOT PAY PENALTIES FOR SKIPPING THEM

One of the most common — and most avoidable — financial mistakes South Florida small business owners make is failing to pay federal quarterly estimated taxes throughout the year and then facing both an unexpected large bill and underpayment penalties when they file.

If you expect to owe $1,000 or more in federal income tax for the 2025 tax year — which is the case for most profitable self-employed individuals and pass-through business owners — you are generally required to make quarterly estimated tax payments. The 2025 quarterly deadlines are: April 15 (for Q1), June 16 (for Q2), September 15 (for Q3), and January 15, 2026 (for Q4). Missing these payments results in an underpayment penalty calculated based on the amount owed and the number of days it was underpaid.

Safe harbor rules provide a path to avoid penalties even if you end up owing more than expected: paying at least 100% of the prior year’s tax liability (or 110% if your adjusted gross income exceeded $150,000 in the prior year) in equal quarterly installments protects you from penalties regardless of your actual 2025 liability.

Florida’s corporate income tax also requires estimated payments if annual liability exceeds $2,500, with quarterly deadlines determined by your fiscal year end.

What to do: If you have not been making quarterly estimated payments for 2025 and you owe more than $1,000, consult your CPA immediately about your exposure and whether making a catch-up payment before the Q4 deadline can reduce your penalty. For 2026, set up automatic estimated payments from the first quarter.

TIP 8: UNDERSTAND FLORIDA SALES TAX — AND AUDIT YOUR COMPLIANCE

Florida’s general state sales tax rate is 6%, with county-level surtaxes ranging from 0.5% to 2.5% depending on location. In Miami-Dade, Broward, and Palm Beach counties, those combined rates vary — and for South Florida businesses selling taxable goods or services, collecting and remitting the correct combined rate is a compliance obligation that does not pause because your business is busy.

Sales tax applies to the sale or rental of tangible goods, some services, and commercial property leases. One frequently misunderstood area: if your business leases commercial space in Florida, your landlord is likely collecting sales tax on your rent as part of your payment — Florida taxes commercial real property leases, though the rate was reduced in recent years. Confirm with your CPA whether you are paying this tax correctly and whether any exemptions apply to your specific situation.

Remote sellers with economic nexus in Florida — more than $100,000 in sales to Florida customers in a calendar year — are also required to collect and remit Florida sales tax, a requirement that catches many out-of-state sellers off guard. If your business sells products online or ships goods to Florida customers, confirm your nexus status.

Sales tax returns (Form DR-15) are filed monthly, quarterly, or annually depending on sales volume. Late filing and late payment both trigger penalties and interest. The Florida Department of Revenue conducts audits, and a sales tax audit can reach back three years of records.

What to do: Review your sales tax collection and remittance process annually. If you have any uncertainty about which of your products or services are taxable, which county rates apply, or whether your filing frequency is correct, schedule a compliance review with your CPA or a Florida sales tax specialist.

TIP 9: EXPLORE FLORIDA’S STATE-LEVEL TAX CREDITS — MANY SOUTH FLORIDA BUSINESSES QUALIFY

While Florida’s most prominent tax advantage is what it does not collect — state personal income tax — the state also offers several specific tax credit programs for businesses that qualify, and South Florida small business owners frequently leave these credits unclaimed simply because they are unaware of them.

The Urban Job Tax Credit Program offers eligible businesses in designated urban areas a tax credit of between $500 and $2,000 per new employee. South Florida’s urban enterprise zones in Miami-Dade and Broward counties make this credit relevant to a meaningful number of businesses expanding their workforce. Credits are applied against Florida corporate income tax.

The Research and Development Tax Credit is available to businesses with qualified research expenses that have also received the federal R&D tax credit. Applications for the 2025 credit allocation opened in March 2025 through the Florida Department of Revenue. If your business conducts product development, software development, engineering work, or other qualifying research activities, this credit deserves investigation.

The Individuals with Unique Abilities Tax Credit allows employers to claim $1 for each hour worked by employees with qualifying physical or intellectual impairments — a smaller but genuine credit that reduces Florida corporate income tax liability for participating employers.

Under the OBBBA at the federal level, domestic research and development expenses paid or incurred in 2025 can now be deducted immediately rather than amortized over five years under the prior TCJA rules — a significant change for any South Florida business investing in innovation, product development, or technology.

What to do: Ask your CPA specifically whether any Florida state tax credit programs apply to your business activities. If your business has grown its workforce, invests in research or development, or employs individuals with disabilities, one or more of these programs may generate a meaningful credit on your state return.

TIP 10: DEDUCT YOUR SELF-EMPLOYED HEALTH INSURANCE PREMIUMS AND HALF OF SELF-EMPLOYMENT TAX

Two deductions that are consistently overlooked by South Florida sole proprietors, single-member LLC owners, and S corporation shareholders deserve specific attention because they directly reduce your adjusted gross income — not just your taxable income — with particularly valuable downstream effects.

Self-employed health insurance premiums are 100% deductible from your adjusted gross income if you pay for health insurance coverage for yourself, your spouse, and your dependents and you are not eligible to participate in a subsidized health plan through an employer (including your spouse’s employer). In South Florida’s private health insurance market, where individual premiums are substantial, this deduction can be significant. The deduction is claimed on Schedule 1 of your Form 1040, not on Schedule C — and it also reduces your QBI calculation, which requires coordination with your CPA to ensure both benefits are optimized.

Self-employment tax — the 15.3% combination of Social Security and Medicare taxes that self-employed individuals pay to cover both the employee and employer portions — generates its own partial deduction. The IRS allows you to deduct half of your self-employment tax (the employer equivalent portion, or 7.65%) from your adjusted gross income when calculating your federal income tax. This deduction appears on Schedule 1 and automatically flows through when you complete Schedule SE correctly.

Both deductions reduce your AGI, which has positive effects on your QBI calculation, your eligibility for other income-tested deductions and credits, and — in Florida — your overall tax profile as a business owner who has structured their affairs to take full advantage of the state’s favorable tax environment.

What to do: Confirm with your CPA that both your health insurance premium deduction and your self-employment tax deduction are being claimed correctly and in the proper location on your return. Ensure that the interaction between these deductions and your QBI calculation is being managed holistically rather than in isolation.

QUICK REFERENCE SUMMARY

Federal deductions and provisions for 2025

- 20% QBI deduction — permanent under OBBBA, phase-out begins at $394,600 (MFJ) / $197,300 (single)

- 100% bonus depreciation — restored permanently for property placed in service after January 19, 2025

- Section 179 deduction — limit raised to $2.5 million, phase-out at $4 million

- Solo 401(k) — up to $70,000 combined contribution limit; $81,250 for ages 60–63

- SEP IRA — up to 25% of compensation or $70,000, whichever is less

- Business meals — 50% deductible with proper documentation

- Mileage — 70 cents per mile (2025 IRS standard rate) with a contemporaneous log

- Health insurance premiums — 100% deductible from AGI for self-employed

- Self-employment tax — deduct 50% of SE tax from AGI

- Domestic R&D expenses — immediately deductible in 2025 under OBBBA

Florida state tax reminders

- No Florida personal income tax on pass-through income (sole proprietors, S corps, partnerships)

- Florida corporate income tax: 5.5% on federal taxable income above $50,000 — applies to C corps and LLCs taxed as C corps

- Florida state sales tax: 6% plus county surtax (verify your county rate)

- Commercial lease tax: verify with your CPA — Florida taxes commercial real property leases

- Estimated tax payments required if annual Florida corporate liability exceeds $2,500

- Urban Job Tax Credit, R&D Tax Credit, and other state credits — ask your CPA if you qualify

Key 2025 filing deadlines

- Q4 2025 estimated tax payment: January 15, 2026

- Individual and pass-through returns: April 15, 2026 (extension available to October 15, 2026)

- Florida corporate income tax: First day of the fifth month after tax year ends

- SEP IRA and Solo 401(k) contributions: Up to the filing deadline including extensions

- SIMPLE IRA: Must be established by October 1 of the applicable tax year

This article is for general informational purposes only and does not constitute legal, tax, or accounting advice. Tax laws are complex and subject to change. Please consult a qualified CPA or tax attorney for advice specific to your business situation.

South Florida Small Business Tax Guide · 2025 Tax Year · Miami-Dade · Broward · Palm Beach 10 Tips for the South Florida Small Business Owner Filing for the 2025 Tax Year